Blog

Is It Worth Hiring a Buyer's Agent When Buying New Construction? (Absolutely Yes)

Alpine Estates Cranston, RI Luxury Homes for Sale | Jason Pacheco, Realtor

Why Hiring a Full-Time Full-Service Realtor in Rhode Island Can Save You Thousands

Reliable Brokers in Cranston, RI to Help You Sell Your Home (2026 Guide)

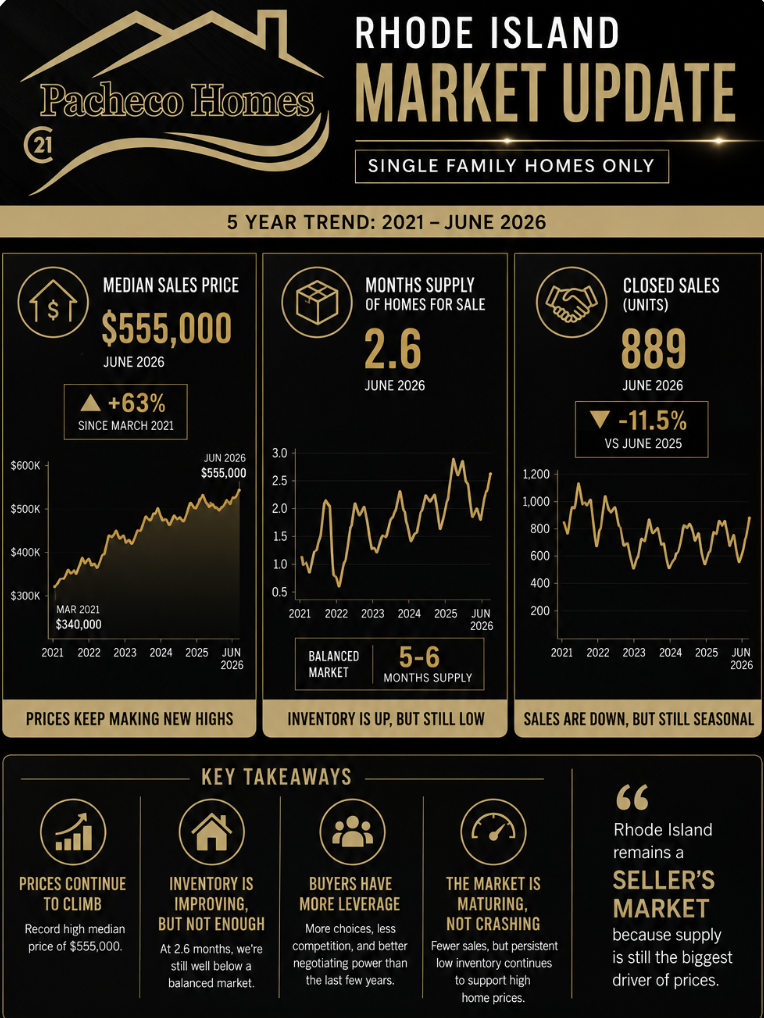

Home Prices Continue to Rise Despite More Homes for Sale If you've been waiting for Rhode Island home prices to fall, the latest housing market data tells a different story. While inventory has improved compared to the historic lows of 2021 and 2022, the market remains firmly in seller territory. Median home prices for single-family homes reached $555,000 in June 2026 , an increase of approximately 63% since March 2021 , highlighting the continued demand for Rhode Island real estate despite higher mortgage rates. One of the biggest misconceptions in today's housing market is that rising inventory automatically means falling prices. In reality, Rhode Island currently has just 2.6 months of housing supply , while a balanced real estate market typically has 5 to 6 months of inventory . Although buyers have more choices than they did during the peak of the pandemic housing boom, there are still not enough homes available to satisfy demand. This ongoing shortage continues to support home values across the state. Another important trend is that closed sales are lower than they were one year ago , but that doesn't necessarily signal a weakening market. Instead, fewer buyers are purchasing homes primarily because affordability has become more challenging with today's mortgage rates. At the same time, many homeowners with low fixed-rate mortgages are choosing not to sell, limiting the number of new listings entering the market. The result is fewer transactions, but continued upward pressure on home prices due to limited supply. For buyers, today's market offers slightly better negotiating opportunities than in recent years. Multiple-offer situations are less common, inspections are becoming more acceptable, and buyers often have a little more time to make decisions. However, well-priced homes in desirable Rhode Island communities continue to attract strong interest and can still sell quickly. For sellers, the data remains encouraging. Home values continue to trend upward, inventory remains historically low, and motivated buyers are still actively searching for homes throughout Rhode Island. Proper pricing, professional marketing, and strategic negotiation remain the keys to maximizing your home's value in today's evolving market. As a local Rhode Island Realtor, I believe the biggest story isn't that the housing market is slowing—it's that the market is maturing . We are moving away from the extreme conditions of 2021 and 2022 and into a healthier, more balanced environment. Unless Rhode Island experiences a significant increase in new housing construction, limited inventory is likely to continue supporting home prices throughout the coming year. If you're thinking about buying or selling a home in Cranston, Cumberland, Lincoln, Warwick, Johnston, North Providence, Smithfield, Coventry, East Providence, or anywhere in Rhode Island , understanding these market trends can help you make confident real estate decisions. Whether you're a first-time home buyer, moving up, downsizing, or selling your current home, having a local market expert can make all the difference. Contact Jason Pacheco with Pacheco Homes Team for a personalized home value estimate, current market analysis, or to discuss your real estate goals in Rhode Island. The market continues to evolve, and having accurate local knowledge is one of the biggest advantages you can have.

Top Realtor in Cranston RI: Your Complete Guide to Buying and Selling a Home in Cranston, Rhode Island - Jason Pacheco Real Estate Agent

Selling your current home while buying your next one at the same time can feel overwhelming. For many homeowners in Rhode Island, this is one of the biggest real estate challenges they face. Common questions I hear from homeowners include: Should I sell first or buy first? What happens if my home sells too fast? What if I find my dream home before selling? How do I avoid carrying two mortgages? Can I make a competitive offer if I still need to sell my current home? The good news? With the right strategy and the right Realtor, selling and buying at the same time can be done smoothly. As a full-time Rhode Island Realtor, I help clients navigate this process every day. Step 1: Understand Your Current Home’s Value Before making any major decisions, you need to know what your current home is worth in today’s market. This gives you clarity on: How much equity you have Your potential down payment Your monthly budget for the next home Your overall buying power Many homeowners are surprised to learn they have more equity than they think. Understanding this number first helps everything else fall into place. Step 2: Decide Whether Selling First or Buying First Makes More Sense There’s no one-size-fits-all answer. It depends on: Your finances Your comfort with risk Current inventory levels Current mortgage rates Your timeline Selling First Selling first offers more financial certainty. Pros: Know exactly how much money you’re working with Avoid two mortgage payments Stronger financial position Cons: May need temporary housing Might feel rushed to buy Buying First Buying first can reduce moving stress. Pros: Secure next home first Easier transition for family Less pressure during move Cons: More financial pressure Possible overlap in mortgage payments A good Realtor helps determine which option fits your situation best. Step 3: Build a Strategic Plan for Timing Timing is everything. This is where experience matters. In Rhode Island, we often help clients with strategies such as: Home Sale Contingencies This allows you to make an offer on a new home contingent on selling your current property. Rent-Back Agreements Sell your home and remain in it temporarily after closing. Same-Day Closings Sell one property and buy the next on the same day. Bridge Financing Access equity before your current home officially sells. These strategies can dramatically reduce stress. Step 4: Prepare Your Current Home to Maximize Value Before listing, we focus on maximizing your sale price. This may include: Pricing strategically Professional photography Minor repairs Decluttering Staging Strong marketing exposure The goal is simple: Create demand. When multiple buyers compete, sellers often gain stronger offers and better terms. Step 5: Work With a Realtor Who Can Coordinate Both Sides This is where everything comes together. Selling and buying at the same time is about more than just transactions. It’s about strategy, negotiation, timing, and risk management. An experienced Realtor helps coordinate: Showings Offers Deadlines Inspections Appraisals Financing Closing timelines Having one clear game plan makes the process much easier. Why Rhode Island Homeowners Need a Strong Strategy Right Now The Rhode Island market remains competitive in many areas including: Cranston Warwick Cumberland Lincoln Smithfield North Providence Inventory is still relatively tight, meaning preparation matters. The homeowners who win are usually the ones with the best plan. Final Thoughts Selling your home and buying another at the same time doesn’t need to be chaotic. With proper planning, the right timing, and strong guidance, the process can be smooth and successful. If you’re thinking about making a move in Rhode Island and want a customized strategy, I’d be happy to help. The first step is simply having a conversation and building a game plan around your goals. Whether you’re upsizing, downsizing, relocating, or buying your forever home, having the right strategy can make all the difference.

Sell and Buy a Home at the Same Time in Rhode Island | Complete Guide for Rhode Island Homeowners

Top Realtor in Cranston RI: Frequently Asked Questions About Buying and Selling Homes in Cranston, Rhode Island

Top Realtor in Cranston – Why Buyers & Sellers Choose Jason Pacheco